Despite Strong Economic Data, Market Rout Friday Causes Stocks and Bonds to Fall

Good morning,

The Dow (-0.3%), NASDAQ (-4.7%), S&P 500 (-2.6%), and EAFE (-1.4%) all fell for the week. Meanwhile, bonds were mixed as taxable bonds fell 0.5% and tax-free municipal bonds gained 0.4%. The 10-year Treasury rose 0.10% to finish the week at 4.54%.

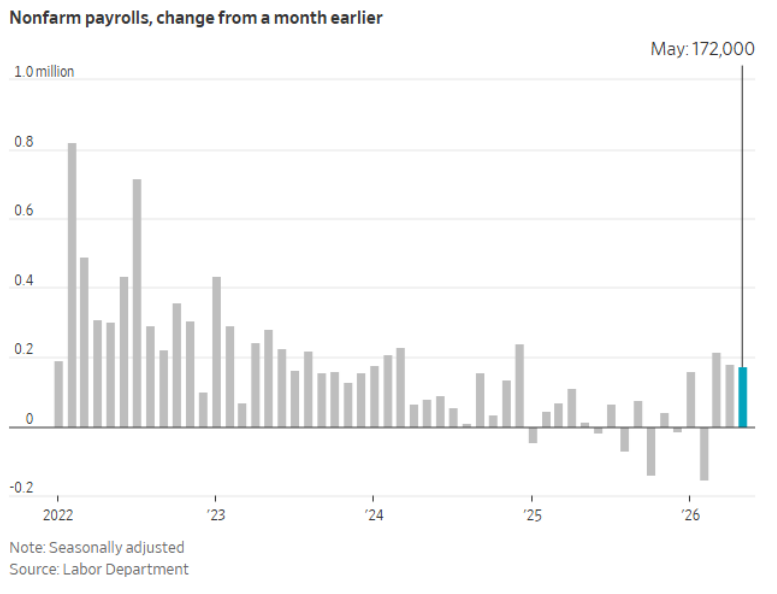

Friday’s sharp losses (2% - 4%) pulled the markets down for the week, ending a 9-week streak of stock gains. The losses on Friday were triggered by a fear of the Fed raising interest rates, and technology stocks (particularly semiconductor stocks) giving back some of its parabolic gains over that period. Many pundits believe that the losses in the tech stocks on Friday are a result of those stocks currently being over bought, along with some profit-taking. The trigger on Friday was the May jobs report, as the US economy added 172,000 jobs, compared to economists’ expectations of 80,000 job gains. The 3-month average job gain was the largest since March 2024. See the chart below that shows monthly job gains / losses since January 2022. Note that the large job gains in 2022 and 2023 were largely a result of the recovery from enormous job losses during COVID in 2020 and 2021.

In short, the market response on Friday was another version of “good news is bad news”, as that report, along with other economic data, caused the bond market to price in a nearly 100% likelihood of a rate hike in 2026, with some chance of it being as much as three hikes. That is in contrast to an expectation of three rate cuts at the start of the year. Rate hikes are designed to cool rising inflation, but not at the mercy of the jobs market, which now appears to be on stronger footing. In other economic news, the Institute of Supply Managers (ISM) Manufacturing and Services reports both exhibited a rise in sentiment, with the manufacturing prices index actually falling, but from already elevated levels. The inflationary pressures are being caused by the Iran conflict, as the oil supply is being restricted, causing fuel prices to rise sharply over the past few months. All eyes will be on two key inflation reports this week – Consumer Price Index (CPI) on Wednesday and Producer Price Index (PPI) on Thursday. These will be very important reports, and will likely trigger market movements if not in line with economists’ expectations.

Have a great day and terrific week!

Source: Yahoo Finance

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index. Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.